1. Introduction

The world was hit by a pandemic during the first half of 2020. Despite the threat and the pressure imposed to the public health, the economic and social disruption will continue having an impact on the long-term existence. Nevertheless, the COVID-19 pandemic had changed all areas of business, including the accounting profession and accounting information systems. The negative effects of the crisis were felt in all areas and they have affected each sector with varying degrees of severity (Kumar, 2020). It is worth mentioning that accounting practices play a key role in organizing modern economic and social life. In both the private and public sectors, many activities are significantly structured around cost-benefit calculations, finance projections, performance and risk assessments, and a mix of other forms of numerical and financial representations. Hence, the accounting information system has a direct impact on the social structure of the business organizations, as well as indirectly in relation to other social institutions, which are important for social and organizational control. Undoubtedly, accounting is an important segment of economics, i.e. economic science, because it facilitates communication between economic entities. The modern trend of globalization is a challenge for both business policy makers and accounting. However, with the development of the world economy, a series of changes and adaptations of two separate economies are required in different areas of economic and social life, all in order to accelerate mutual economic, cultural, political and any other type of cooperation. Therefore, the spread of COVID-19 results in a significant slowdown in every economic activity. This pandemic had severely affected the labor markets, every country’s economy and its enterprises, including global supply chains, leading to widespread business disruption. Without consideration, all industries were affected by the COVID-19 pandemic, with some having stronger defense mechanisms, while the others have been struggling to adjust to the new normality. Nowadays, consumer demand patterns are changing, the global supply chains are being disrupted and have been under much pressure. All these changes have pressured different regions, markets and governments to find ways to respond to the corona crisis. Therefore, on a global level, in order to find an exist from this situations, every company must constantly and quickly adapt to the new and uncertain market conditions (Jabin, 2021).

2. The Global Economic-Financial Crisis and Governance with Crisis Caused by COVID-19

The global economic activity as a result of the negative effects of the COVID-19 pandemic and the restrictive measures taken to prevent further spread of the virus have had a strong adverse effect on the global economic activities, both in developed and developing countries. The COVID-19 pandemic was first identified in December 2019 in Wuhan, China. More specifically on January 30th, the World Health Organization declared a situation of public health concern, followed by a declaration of pandemic on March 11th 2020. The pandemic has resulted in significant global social and economic disruption, including the largest global recession since the Great Depression. This has led to widespread supply shortages exacerbated by panic buying, agricultural disruption, and food shortages. Numerous educational institutions and public areas have been partially or completely closed, and many events have been canceled or postponed (Verschuur, et al., 2021). Hence, with the COVID-19 pandemic, countries entered a recession and experienced major economic crises. To many, the news of the collapse of the world stock markets, the collapse of large companies, the bankruptcy of banks and insurance companies seemed unrealistic. In fact, after many years of prosperity and development, the corona crisis in the world economy came as a shock. The travel industry was severely damaged, with all airlines suspended, people forced to cancel business trips and vacations. The catering sector was also severely affected, with millions of jobs lost and many bankrupted companies. The obtained data from Transparent, a leading intelligence industry company covering more than 35 million hotel and rental listings worldwide, has seen bookings drop in all top travel destinations. Most small businesses do not have the cash reserves to survive a one-month break, and forecasts suggest there will be a significant increase in the number of workers who could lose their jobs in just one week because of the pandemic. On one hand, it can be noted that from the COVID-19 crisis, mostly affected sectors are the tourism, catering sectors, transport, accounting, investments in construction, crafts, and many others. On the other hand is the increase of e-commerce and online sales during the pandemic. Due to the significant reduction and imbalance between supply and demand, economies faced strong shocks and weakened the resistance of businesses. While the demand for certain products and services has increased dramatically (medical equipment, electronic communication platforms, electronic payments, etc.), the demand for other products and services (tourism and hospitality, automotive industry, etc.) has decreased significantly. The transport sector is facing serious difficulties because of the newly imposed protection measures in each country. State budget revenues will not be sufficient to meet expenditures and expenditure requirements and this situation leads the countries to a larger budget deficit than originally planned. The population is not resistant to the financial crisis, given the already low-income levels. This situation again puts the population at risk of poverty, thus, stakeholders should refrain from procurement and investment so that economic growth will be negative or remain the same (Amutha, 2021).

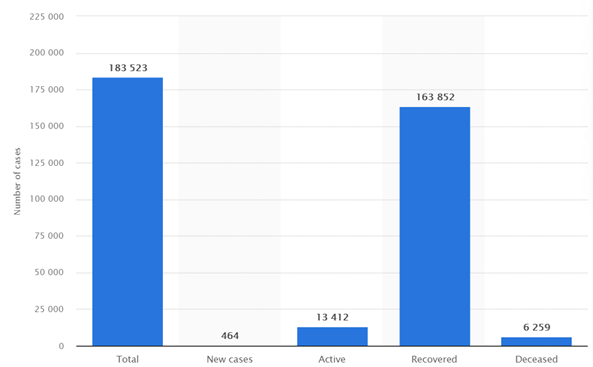

Furthermore, in this paper a descriptive analysis has been conducted for the period since the occurrence of the corona pandemic up until today. The data for the analysis was obtained from Statista website, with a country of interest being N. Macedonia. The analysis included the total number of cases, GDP growth and the Accountants performance. In Figure 1 are presented the total number of cases in N. Macedonia until September 2021. These numbers are of importance, because every person who got in touch with the virus was in isolation for minimum ten days. These measures deeply affected the businesses and consequently imposed burdens on accountants to complete their activities. Not only that every corona active person was isolated, due to the restrictions, many businesses were closed and many people were laid off. Considering that accountants in N. Macedonia are mainly responsible for preparing the salaries, the whole situation with deregistration of the employees in the Agency for employment pressurized the accountants. According to the Western Balkans Democracy Initiative (2021), the number of unemployed people during the corona crisis, was reduced by 25.545 people or 3.1%, from the total number of employed people. The data shows that only Lithuania and Montenegro had higher unemployment rates than Macedonia in 2020.

Figure 1. Total number of cases until September 2021

Source: Statista website (2021)

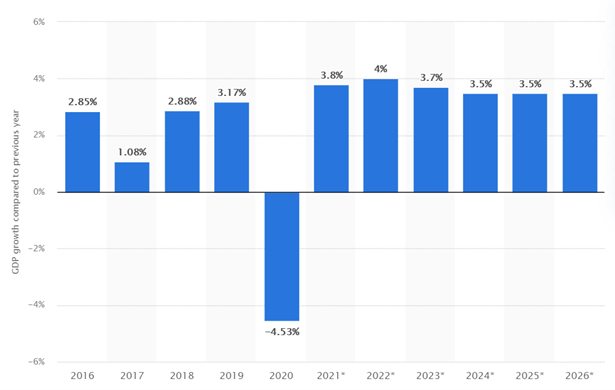

In Figure 2 it can be seen that in 2020, when the corona occurred and the lockdown measures started to be implemented, the GDP in N. Macedonia was severely negatively affected. The price bubbles that were created, especially in the food industry, the excessive leverage, the slowed down economic activities created a sudden drop in the demand, as well as the supply side. Hence, considering that the financial markets are globally interconnected and integrated, all of the economic difficulties around the world had a negative effect in the Macedonian market. According to the Western Balkans Democracy Initiative (2021), the GDP drop in 2020 has been the worst one since the past several decades. It is believed that, the crisis caused by COVID-19 will be shorter and smaller compared to the crisis caused by the transition in the early 1990’s. In Q2 in 2020, the drop in GDP was among the highest in Europe (-14.9%).

Figure 2. GDP growth in N. Macedonia 2016-2026*

Source: Statista website (2021)

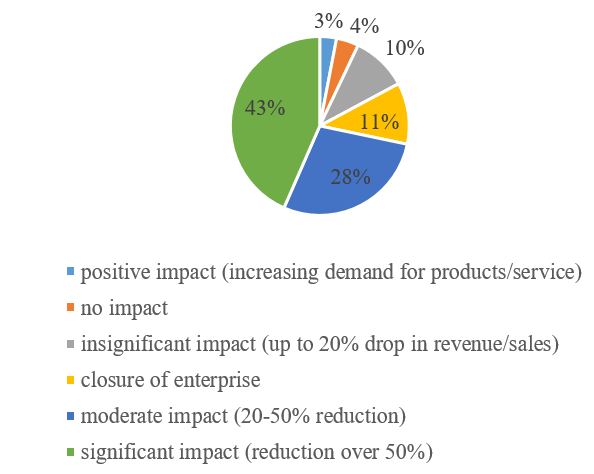

From Figure 3 it can be seen that the corporate revenues were significantly affected by the pandemic. Only 3% od the businesses claimed that they had experienced an increased demand for their product/services, 4% said that the pandemic had no effect at all, 10% said that there has been drop of around 20% in their revenues/sales, 11% have closed their business, 28% said that the pandemic has a moderate impact, while 43% said that the corona crisis contributed to a decrease of over 50% in their revenues.

Figure 3. The impact of COVID-19 on corporate revenues

Source: Author’s calculation

Additionally, many CEOs face declining sales and revenues and increased costs. Adaptation interventions may require investment in key technologies, processes, and people. Although the focus of all economic and financial theorists lately is the global economic and financial crisis that is a result of the current state of the overall social environment, it is still not the only problem that businesses can face. For some, liquidity has become a matter of survival. Management or management crisis, market-development crisis, social or organizational-legal crisis are a constant threat to business entities. On one hand, the crisis itself brings many threats to the successful operation and development of the business entities, but on the other hand, it is a chance to eliminate all irrationalities in operations, to increase economic activities, which consequently creates a stable basis for future economic development. This is because in times of crisis, all the shortcomings of economic-organizational-technical nature come to the surface and become a burden on the business entity, the release of which increases its chances of survival and successful overcoming of crisis of any nature.

3. Adequate Organization of the Accounting-Information System of Business Entities During COVID-19

The accounting systems of many countries in the world are affected by the process of globalization caused by COVID-19. In this sense, this process has an appropriate impact on accounting and financial reporting. The globalization caused by COVID-19 is a phenomenon of total changes in the world, changes in operations and changes in information requirements. It is generally accepted that accounting contributes to the economic development and progress of the national, regional and world economies. Without accounting, more specifically, accounting information, the vital systems of any country cannot function. This improper functioning affects the tax system, national income statistics, Gross domestic product, etc. The growing internationalization of world business imposes the need to study the accounting systems of individual countries and the action of certified public accountants on the world stage, providing services to companies in international business (Besuspariene, 2018). In terms of COVID-19, accounting and accounting information systems gained new dimensions and features. Integrated management of the goals, strategies and performance of enterprises is a result of new challenges and management solutions in increasingly complex operating conditions, with the necessary appropriate accounting - information support. The response of accountants - financial and managerial, to these management requirements was the concept of integrated reporting for the needs of management in successful realization of the goals, strategy and performance of the modern enterprise. Furthermore, the management team of any enterprise is obliged to successfully complete all of the management activities or functions, such as planning, organizing, execution, motivation, leading, control and communication. Moreover, in the domain of strategic and operational goals and tasks, especially in terms of generating, measuring, distributing values for owners, shareholders and other stakeholders, the management of the company, in addition to intuition, experience and personal recognition, has a need for appropriate quality information support. In that sense, the accounting information system with its quality basis (database) makes the basic part of the overall business information system. Within each business entity there are different information systems that are interconnected and aimed at achieving the goal for which the business entity was established, which is reflected in the maximization of overall business performance. The production information system, the personnel information system, the accounting information system are just some of the information subsystems that exist within each business entity. Globally, the information system within the business entity can be divided into three main subsystems whose existence is implied within each business entity. The first is a management-information subsystem that includes all levels of management, from the lowest to the highest management, whose role is to make decisions from a strategic to a tactical nature. The accounting-information subsystem is a database of each business entity and a stable information base for decision-making within the business entity. Although this subsystem is largely oriented towards the past, it provides anticipation of future business movements based on the past, creating a reliable basis for the future functioning of the business entity. The third, but no less important subsystem is the production-information subsystem within which the functions such as production, procurement, sale, etc. are located, and through which the activity of each business entity is realized. Depending on the organizational structure of each entity separately, each of these information subsystems can function as a stand-alone information system or as part of an integrated information system. The accounting information system is the oldest information system in every business entity. This system contains and provides the necessary information for recording business transactions, valuation of resources and performance, decision making as well as reporting. In order to fulfill its role, it must cooperate with all other information systems in the business entity. The purpose of the accounting information system is reflected in the provision of information of a certain quality and quantity intended for the needs of different users. In order to meet the requirements that the modern market environment sets before the accounting-information system, it is necessary to constantly improve it. First, modern information technology must be implemented in the accounting information system, which enables faster and more efficient data processing, as well as greater efficiency of the overall accounting information system. This is mainly achieved through an integrated accounting-information system which actually unites a number of modules in a single accounting-information system which ensures that all data in it is entered only once and used in further processing procedures. This system is based on on-line access. The above indicates the importance of the successful organization of the accounting and information system, which was especially evident in times of crisis, when the rapid response to market trends is an imperative for the survival of the business entity in changing market conditions. Businesses with a well-organized information system in such times ensured their survival by timely anticipation of negative market trends and adequate response to them (Farida, et al., 2021).

4. Challenges to the Accounting-Information System in Relation to the Current Economic and Financial Crisis

The key step for all these changes in accounting is: there is no going back. That's a good thing. There are many benefits of working from home - it reduces travel time, eliminates overhead costs and gives your team members the freedom to work whenever they want. Therefore, the imposed question is if it id the right option for everyone? Some prefer to work in an office, however, giving people the opportunity and freedom to work wherever they want, whenever they want, makes the employees happier, more loyal and more productive. COVID-19 has proven that the company does not stop when the physical office closes, so the profession needs to embrace that forward-looking change. Another thing that was noticed during the pandemic is that clients are just as adaptable as the accounting firms are. Clients may have thought that they would never try a zoom meeting or would have ever figured out how to join one. Since the occurrence of the corona pandemic, they figured out how to safely upload documents and sign a document electronically (Teodorovicz, et al., 2021). The functioning of each business entity is successful only insofar as its organizational structure is based on interdependence and feedback from its parts and the whole. The system set up thus enables doing business activities with better results and lower costs. Firstly, the accounting information system is tasked to identify all the negative effects of the crisis, and later, the accounting information system is expected to be the primary mechanism for overcoming it. A special challenge for the accounting information system is to provide a high degree of reality to the financial statements, as they are in fact the information base for making business decisions of the company. In order to ensure trust and quality improvement in the electronic updating of the complete documentation of a company and to enable efficient financial reporting, the accounting information system should be properly organized. In that direction, high efficiency of the overall accounting function must be achieved with adequate integration of human and material resources within the accounting. Raising the awareness and ethical responsibility of accountants on the importance of real financial reporting is one of the measures on the way to improving the quality of accounting information systems. Within the accounting function, in the future more attention should be paid to accounting planning, as a segment of the accounting-information system oriented towards the future. Namely, through the accounting information system, a signal should be sent in time to the management for all potential negative market implications on the business entity and to take the necessary measures in time to overcome them. This enables fast action and avoidance of the certain consequences that the economic-financial crisis caused by COVID-19 brings on the operation and survival of the business entities (Lin and Hwang, 2021).

5. Improvements Needed for Better Organizing the Accounting Information System

Good accounting information system can improve the financial performance of the companies and their accountability. Therefore, its quality should be measured based on its reliability, relevance, clarity and accuracy (Hezabr, 2018). Hence, creating good decision-making process requires higher standards of accounting information system’s quality. Therefore, better organizing the accounting information system should be one of the key task for every company. The imposed question is how the necessary changes and improvements should be conducted. One of the key measures is to continuously work on improvements, not only on the methods used, but on improvement of the people who provide the accounting service as well. Fitrios (2016) claims that quality accounting information system generates accounting information quality. Consequently, the quality of accounting information improves the profitability and managerial efficiency of the businesses (Kanakriyah, 2016). It is worth mentioning that for better organizing the accounting information system, the quality of the organization’s internal factors play important role. Those factors include the humans and the equipment. Additionally, the infrastructure factors, the knowledge and the dedication of the accountants, as well as the leadership support can improve the accounting information system (Thoa and Van Nhi, 2020). Nevertheless, these are some general factors that can have an impact, but every organization has its unique accounting information system and should incorporate methods that will be most adequate to its characteristics. For example, one organization may work more on improving the accountants’ knowledge, other may be more focused on other internal or external factors. Thus, depending on the issue, the adequate method and strategy should be used. Some organizations may focus more on the human resources, while others will focus more on the technical systems, such as communication technology, software or hardware. According to Xu, et al. (2003), the quality of the financial accounting information system depends on the application of software and hardware equipment. This application assist in the process of collecting and storing data in more effective and efficient way. Furthermore, Internet is also useful method for exchanging and connecting data among different departments (Taylor, et al, 2007). Finally yet importantly, financial contribution to the people in the organization contributes to better performance and dedication in performing the tasks. Hence, the financial factor, as well as the support from the leadership improve the function and the performance of the people who provide the accounting services (Thoa and Van Nhi, 2020).

6. Conclusion

In the current crisis and changing global market conditions, running a business is becoming increasingly difficult and uncertain. Effective management of the mission, goals, strategies and performance of enterprises is becoming more complex, with greater demands and with pronounced characteristics of interdisciplinary and multidisciplinary, with a pronounced need for new knowledge, skills and competencies. Businesses in times of crisis must immediately take certain measures to ensure their own survival. These measures primarily refer to the reorganization of operations, improving the overall economy and efficiency of the operations, as well as radical changes in overall operations. Significant support in the implementation of these tasks is provided by the accounting-information system that has a dual role. It should be the first to point out the negative market trends for the business entity, and on the other hand to provide a reliable information base for making business decisions that will be an appropriate response to the given market trends. In order for the accounting-information system to successfully perform these tasks, it is required to constantly improve its organization, as well as to provide quality staff to accomplish these tasks. Without well-organized and highly qualified human resources, the accounting-information system cannot meet the challenges it faces.

6. References

Amutha, D. (2021). Impact of COVID-19 on various sectors of the economy. St. Mary’s College, Tuticorin.

Besuspariene, E. (2018). The importance of financial accounting information for Business Management. Accounting, audit and forensic science, p.75-81.

Farida, L.; Mulyani, S.; Akber, B.; Setyaningsih, S. D.; Quality and efficiency of accounting information systems. Utopia y Praxis Latinoamericana. Vol. 26, No. 2.

Fitrios, R. (2016). Factors that influence accounting information system implementation and accounting information quality. International Journal of Scientific and Technology Research, Vol. 5 No. 5, pp. 192-198.

Hezabr, A. A. (2018). Improving accounting information systems to facilitate supply chain management. European Journal of Accounting, Auditing and Finance Research, Vol. 6, No. 6, p. 44-51.

Jabin, S. (2021). The impact of COVID-19 on the Accounting Profession in Bangladesh. Journal of Industrial Distribution & Business. Vol. 12, No. 7, p. 7-14.

Kanakriyah, R. (2016). The effect of using accounting information systems on the quality of accounting information according to users perspective in Jordan. European Journal of Accounting, Auditing and Finance Research, Vol. 4 No. 11, pp. 58-75.

Kumar, M. M. (2020). The World after COVID-19 and its impact on Global Economy. Leibniz Information Centre for Economics. Retrieved from: https://www.econstor.eu/handle/10419/215931

Lin, H. & Hwang, Y. (2021). The effects of personal information management capabilities and social psychological factors on accounting professionals’ knowledge-sharing intentions: pre and post COVID-19. International Journal of Accounting Information Systems. Vol. 42.

Statista website (2021). Data. Statista website. Retrieved from: https://www.statista.com/

Taylor, J.; Lips, M; Organ, J; (2007). Information-intensive government and the layering and sorting of citizenship, Public Money and Management, Vol. 27 No. 2, pp. 161-164.

Teodorovicz, T.; Sadun, R.; Kun, A. L.; Shaer, O.; (2021). Working from home during COVID-19: evidence from time-use studies. Harvard Business School. Retrieved from: https://www.hbs.edu/ris/Publication%20Files/21-094_d4978fbf-11ea-49aa-bb88-09d39e88a272.pdf

Thoa, D. T. K. and Nhi, V.V. (2020) Improving the quality of the financial accounting information through strengthening of the financial autonomy at public organizations. Journal of Asian Business and Economic Studies, Vol. 29, No. 1, p. 66-82.

Verschuur, J; Koks, E. E., Hall, J. W. (2021). Global Economic impact of COVID-19 lockdown measures stand out in high-frequency shipping data. Institute for Advanced Sustainability Studies.

Western Balkans Democracy Initiative (2021). Inequality in time of corona. The effects of the COVID-19 pandemic on the Macedonian economy. WFD website. Retrieved from: https://www.wfd.org/wp-content/uploads/2020/09/Efektite-od-Kovid-vrz-MK-ekonomija-MK-2.pdf

Xu, H; Nord, J.H; Nord, G.D; Lin, B. (2003). Key issues accounting information quality management: Australian case studies, Industrial Management and Data Systems, Vol. 103, pp. 461-470.